SOC 2 • Fintech Vendors • Bank Security Reviews • Evidence Readiness • Financial Services

Checklist: Evidence Banks Expect from Fintech Vendors During SOC 2 Readiness

Banks do not only ask whether a fintech vendor is “working on SOC 2.” They want proof. During vendor due diligence, banks expect clear evidence for access control, API security, data protection, vendor risk, incident response, business continuity, change management, logging, and governance.

Quick Snapshot

| Evidence Area | Why Banks Ask |

|---|---|

| Access Control | Banks want proof that customer and financial data is protected from unauthorized access. |

| API Security | Fintech integrations often depend on secure APIs, tokens, scopes, and monitoring. |

| Availability | Banks need confidence that critical services can stay reliable and recover quickly. |

| Processing Integrity | Financial workflows must be complete, accurate, valid, timely, and traceable. |

| Vendor Risk | Banks want to know which third parties support the fintech service. |

| Governance | Banks expect risk ownership, policies, management review, and security accountability. |

Introduction

Fintech vendors face tough security reviews.

Banks ask detailed questions before approving a vendor, partner, API integration, platform, payment workflow, data exchange, or embedded finance relationship.

They may ask for:

SOC 2 readiness roadmap

Security policies

MFA evidence

Admin access reviews

API security controls

Incident response plan

Backup and recovery evidence

Vendor register

Risk register

This can feel overwhelming for a fintech team. But the bank is not trying to create paperwork for no reason. Banks need to protect customer trust, financial data, operational resilience, regulatory expectations, and third-party risk.

If your fintech company is preparing for SOC 2, you need an evidence bank before the bank asks.

This checklist explains the evidence banks often expect from fintech vendors during SOC 2 readiness and how to organize it before procurement pressure slows the deal.

Need SOC 2 Evidence for Bank Vendor Reviews?

Canadian Cyber helps fintech vendors prepare SOC 2 evidence banks, API security control packs, SharePoint evidence workspaces, vendor risk registers, incident response plans, and bank-ready trust summaries.

Why Banks Ask for Evidence During SOC 2 Readiness

Banks manage third-party risk carefully. A fintech vendor may touch customer data, account information, transaction records, payment workflows, identity data, API integrations, financial reporting, fraud signals, support tickets, logs, and sensitive business data.

If that fintech vendor has weak security, the bank may inherit risk.

| Bank Concern | Evidence They May Request |

|---|---|

| Can unauthorized users access data? | MFA reports, access reviews, offboarding evidence. |

| Can APIs be abused? | API authentication, rate limits, token controls. |

| Can the service stay available? | Uptime monitoring, backup and recovery evidence. |

| Can transactions be trusted? | Processing integrity checks, reconciliation evidence. |

| Are vendors managed? | Vendor register, assurance reports, sub-processors. |

| Can incidents be handled quickly? | Incident response plan, tabletop evidence. |

| Are changes controlled? | Pull requests, approvals, deployment records. |

| Is leadership accountable? | Risk register, management review, policy approvals. |

Practical rule: Banks trust fintech vendors faster when security answers are evidence-backed.

Evidence Category 1: SOC 2 Status and Readiness Roadmap

If your SOC 2 report is not complete yet, banks may still want to see your readiness plan. Do not answer with only, “We are working on SOC 2.” That is too vague.

| Better Evidence | Purpose |

|---|---|

| SOC 2 readiness roadmap | Shows timeline and control focus. |

| Scope statement | Defines product, systems, data, and services in scope. |

| Trust Services Criteria selection | Shows whether Security, Availability, Processing Integrity, Confidentiality, or Privacy apply. |

| Gap assessment summary | Shows known gaps and remediation plan. |

| Control owner matrix | Shows accountability. |

| Evidence tracker | Shows evidence collection progress. |

Strong bank response:

“We are preparing for SOC 2 and have completed scope definition, gap assessment, control owner assignment, and evidence collection planning. Our readiness work focuses on access control, API security, vendor risk, incident response, backup recovery, change management, logging, and processing integrity.”

Evidence Category 2: Access Control Evidence

Access control is one of the first areas banks review. They want to know who can access systems, customer data, APIs, production infrastructure, support tools, and admin consoles.

| Access Evidence | Why It Matters |

|---|---|

| MFA report | Shows strong authentication. |

| Admin access review | Shows privileged access is reviewed. |

| User access review | Shows access is appropriate. |

| Offboarding samples | Shows access is removed when people leave. |

| Service account register | Shows non-human accounts are owned. |

| Support access review | Shows customer data access is controlled. |

| Access approval records | Shows new access is authorized. |

| Exception register | Shows deviations are approved and monitored. |

Common bank questions:

- Do you enforce MFA?

- How often is access reviewed?

- Who has production access?

- How is access removed after termination?

- Can support staff access customer data?

- Are service accounts reviewed?

Practical rule: Banks do not just want to hear that access is controlled. They want proof.

Prepare Your Access Control Evidence Before the Bank Review

Canadian Cyber helps fintech vendors organize MFA evidence, admin access reviews, service account registers, support access reviews, offboarding samples, and access exception registers.

Evidence Category 3: API Security Evidence

Fintech vendors often connect to banks through APIs. That makes API security a major due diligence area.

| API Security Evidence | Why It Matters |

|---|---|

| API authentication standard | Shows how clients authenticate. |

| API scope matrix | Shows permissions are limited. |

| Token lifecycle procedure | Shows creation, rotation, revocation, and expiry. |

| API key review | Shows stale keys are removed. |

| Rate limit configuration | Shows abuse prevention. |

| API gateway rules | Shows traffic control. |

| Failed authentication monitoring | Shows attack visibility. |

| Webhook signing standard | Shows payload integrity. |

| API abuse runbook | Shows response process. |

Common API risks banks care about:

Long-lived API keys

No key rotation

Weak tenant separation

Unmonitored API failures

Missing rate limits

Insecure webhooks

Poor logging

Practical rule: For fintech vendors, API controls should be part of the SOC 2 evidence bank from day one.

Evidence Category 4: Data Protection and Encryption Evidence

Banks need confidence that financial and customer data is protected.

| Data Protection Evidence | Why It Matters |

|---|---|

| Data flow diagram | Shows where sensitive data moves. |

| Data classification summary | Shows data types and sensitivity. |

| Encryption at rest evidence | Shows stored data protection. |

| Encryption in transit evidence | Shows secure transmission. |

| Key management procedure | Shows how keys are protected. |

| Secrets vault evidence | Shows secrets are not stored insecurely. |

| Data retention policy | Shows how long data is kept. |

| Tenant separation design | Shows customer data boundaries. |

Practical rule: If the fintech handles bank or customer data, data flow and encryption evidence should be easy to produce.

Evidence Category 5: Availability and Resilience Evidence

Banks care about uptime. They also care about recovery. If your API or platform supports bank workflows, availability evidence matters.

| Availability Evidence | Why It Matters |

|---|---|

| Uptime report | Shows service reliability. |

| Monitoring configuration | Shows visibility. |

| Alert rules | Shows detection capability. |

| On-call schedule | Shows response ownership. |

| Incident tickets | Shows issues are tracked. |

| Backup reports | Shows backups are running. |

| Restore test evidence | Shows recovery is tested. |

| Dependency map | Shows critical vendors and systems. |

Common bank questions:

- How do you monitor uptime?

- What happens during an outage?

- Are backups tested?

- Do you have recovery objectives?

- Which vendors affect availability?

- How are customers notified?

Practical rule: A backup report is not enough. Banks often want restore test evidence.

Evidence Category 6: Processing Integrity Evidence

Processing Integrity is especially important for fintech vendors. Banks want to know whether transactions, workflows, calculations, and data transfers are complete, accurate, valid, timely, and authorized.

| Processing Integrity Evidence | Why It Matters |

|---|---|

| Input validation standard | Shows bad data is rejected. |

| Transaction trace samples | Shows records can be traced. |

| Reconciliation reports | Shows outputs match expected results. |

| Duplicate prevention controls | Reduces double-processing risk. |

| Error handling procedure | Shows failures are managed. |

| Failed job review | Shows processing issues are reviewed. |

| Webhook delivery logs | Shows event delivery status. |

| Processing exception tracker | Shows issues are resolved. |

Common bank questions:

- How do you prevent duplicate transactions?

- How do you validate API requests?

- How are failed transactions handled?

- Can you trace a transaction end to end?

- Do you reconcile processed records?

- Are webhook failures monitored?

Practical rule: Processing Integrity evidence is critical when fintech workflows affect financial outcomes.

Evidence Category 7: Vendor and Sub-Processor Evidence

Banks want to know which vendors support your service. This includes cloud providers, payment processors, KYC vendors, fraud tools, analytics platforms, support tools, monitoring tools, and AI vendors.

| Vendor Evidence | Why It Matters |

|---|---|

| Vendor register | Shows supplier visibility. |

| Critical vendor list | Shows high-risk dependencies. |

| Vendor risk reviews | Shows due diligence. |

| Vendor assurance reports | Shows SOC 2, ISO 27001, or security evidence reviewed. |

| DPA / contract tracker | Shows legal and privacy support. |

| Sub-processor list | Supports bank transparency. |

| Vendor remediation tracker | Shows issues are followed up. |

Practical rule: Vendor evidence should show not only who the vendor is, but why they are trusted.

Evidence Category 8: Incident Response Evidence

Banks expect fintech vendors to be prepared for incidents. An incident plan sitting in a folder is not enough.

| Incident Response Evidence | Why It Matters |

|---|---|

| Incident response plan | Shows response structure. |

| Incident role matrix | Shows ownership. |

| Escalation contacts | Shows who is contacted. |

| Bank/customer notification process | Shows communication readiness. |

| Tabletop exercise report | Shows the plan was tested. |

| Lessons learned | Shows improvement. |

| Corrective action tracker | Shows follow-up. |

Incident scenarios to test:

Payment workflow disruption

Bank integration outage

Data exposure

Vendor breach

Ransomware

Processing error

Cloud outage

Practical rule: Banks trust tested incident response more than untested policies.

Prepare a Bank-Ready Incident Response Pack

Canadian Cyber helps fintech vendors create incident response plans, tabletop scenarios, notification workflows, corrective action trackers, and bank-ready incident evidence.

Evidence Category 9: Change Management Evidence

Fintech changes can affect API behavior, transaction handling, security controls, and customer workflows. Banks want to know that changes are reviewed.

| Change Evidence | Why It Matters |

|---|---|

| Change management procedure | Shows rules. |

| Pull request approvals | Shows technical review. |

| Deployment records | Shows release traceability. |

| Test results | Shows validation. |

| Emergency change records | Shows urgent changes are controlled. |

| Rollback plan | Shows recovery planning. |

| Data mapping change review | Supports processing integrity. |

Practical rule: For fintech vendors, change evidence should show security and processing impact were considered.

Evidence Category 10: Logging and Monitoring Evidence

Banks want visibility into security events and operational issues. Logs should support security, availability, and processing investigations.

| Logging Evidence | Why It Matters |

|---|---|

| Log source inventory | Shows what is collected. |

| Log retention setting | Shows investigation support. |

| Access to logs review | Protects sensitive records. |

| Alert rules | Shows detection logic. |

| Monthly alert review | Shows monitoring occurs. |

| API error monitoring | Supports availability. |

| Transaction event logging | Supports traceability. |

| Incident-linked log samples | Shows investigation ability. |

Evidence Category 11: Governance and Leadership Evidence

Banks want to know that security is managed, not improvised.

| Governance Evidence | Why It Matters |

|---|---|

| Risk register | Shows security risks are tracked. |

| Management review minutes | Shows leadership oversight. |

| Policy library | Shows approved security expectations. |

| Control owner matrix | Shows accountability. |

| Corrective action register | Shows remediation tracking. |

| Security roadmap | Shows improvement plan. |

| vCISO report | Shows executive-level security leadership. |

Practical rule: Governance evidence shows that security is part of how the fintech operates.

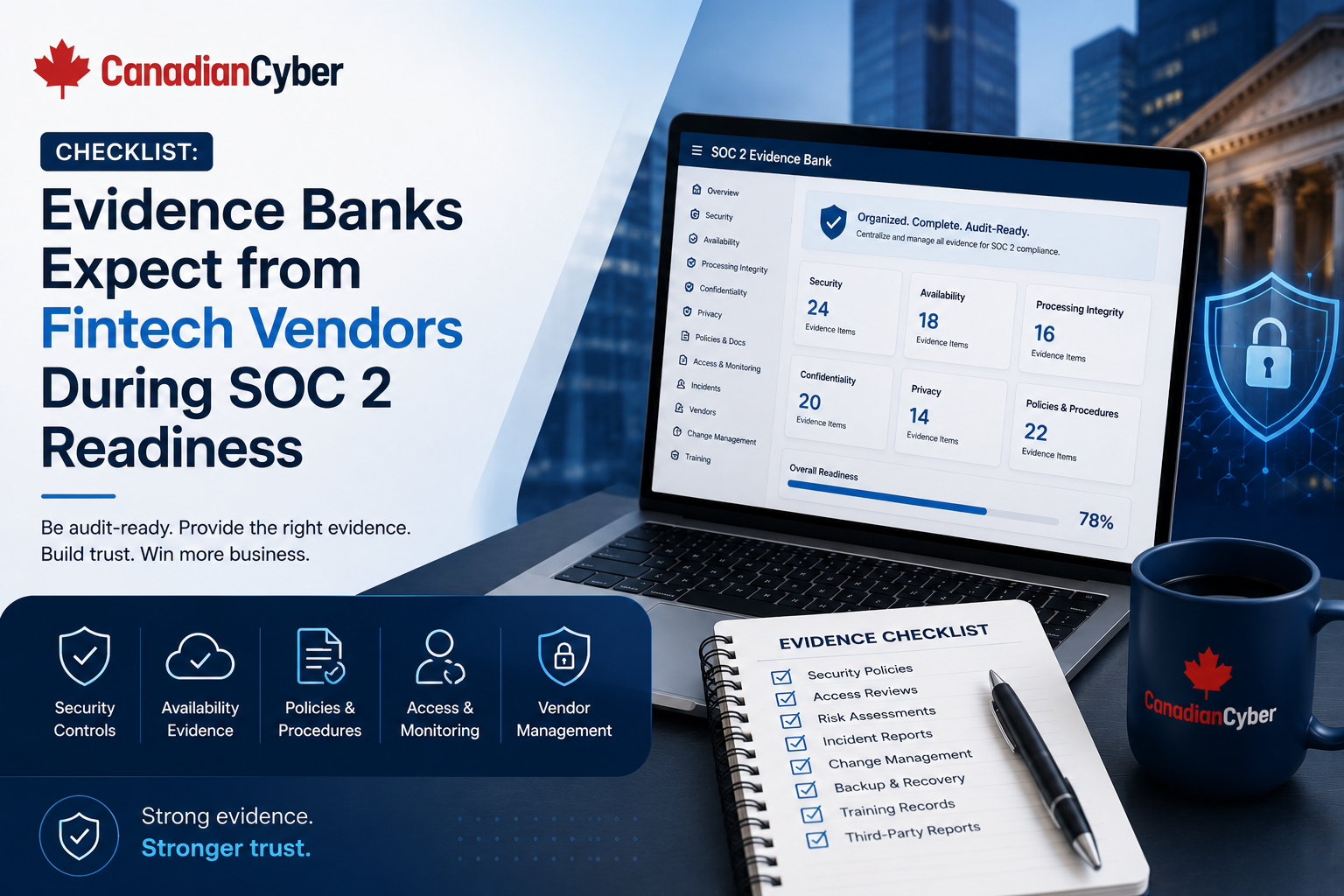

Bank-Ready SOC 2 Evidence Bank Structure

A fintech evidence bank should be easy to navigate. Use clear folders, libraries, metadata, owners, and review statuses.

| Area | Evidence |

|---|---|

| 01 SOC 2 Roadmap | Scope, criteria, readiness plan, gap assessment. |

| 02 Access Control | MFA, access reviews, offboarding, service accounts. |

| 03 API Security | Tokens, scopes, rate limits, webhooks, abuse monitoring. |

| 04 Data Protection | Encryption, data flow, retention, deletion. |

| 05 Availability | Uptime, monitoring, backups, restore tests. |

| 06 Processing Integrity | Validation, reconciliation, error handling. |

| 07 Vendors | Vendor register, assurance reviews, sub-processors. |

| 08 Incident Response | Plan, tabletop, lessons learned. |

| 09 Change Management | PRs, deployments, approvals. |

| 10 Logging | Log sources, alerts, reviews. |

| 11 Governance | Risk register, policies, management review. |

| 12 Bank Trust Pack | Approved summaries and NDA-ready evidence index. |

Build My Bank-Ready SOC 2 Evidence Bank

Canadian Cyber helps fintech vendors build bank-ready SOC 2 evidence banks in SharePoint so security, availability, processing integrity, and governance evidence are ready before procurement pressure starts.

SharePoint Evidence Workspace for Fintech Vendors

A structured SharePoint workspace can help fintech vendors manage evidence without relying on email or random folders.

| Metadata Field | Purpose |

|---|---|

| Evidence Name | Clear title. |

| Control Area | Access, API security, availability, processing integrity. |

| SOC 2 Criteria | Security, Availability, Processing Integrity. |

| Evidence Owner | Person accountable. |

| Source System | Entra ID, GitHub, Jira, cloud, API gateway. |

| Period Covered | Month, quarter, year. |

| Review Status | Requested, uploaded, approved, rejected. |

| Sensitivity | Internal, NDA-only, bank-review, auditor-only. |

| Audit Request ID | Links to bank or auditor request. |

Useful SharePoint views include:

SOC 2 Security evidence

Availability evidence

Processing Integrity evidence

Evidence by owner

Evidence due this month

NDA-only evidence

Auditor-ready evidence

Explore the ISMS SharePoint Solution

Canadian Cyber’s ISMS SharePoint solution helps fintech vendors manage SOC 2 evidence, bank security requests, API controls, risks, vendors, policies, and audit readiness in one Microsoft 365 workspace.

Fintech Vendor SOC 2 Evidence Checklist

Use this checklist before a bank review.

SOC 2 Readiness

| Question | Yes / No |

|---|---|

| Is SOC 2 scope documented? | |

| Are Trust Services Criteria selected? | |

| Is a readiness roadmap available? | |

| Are control owners assigned? | |

| Is the evidence tracker active? |

Access and API Security

| Question | Yes / No |

|---|---|

| Is MFA evidence available? | |

| Are admin access reviews completed? | |

| Are API tokens reviewed? | |

| Are scopes documented? | |

| Are rate limits evidenced? | |

| Are webhook controls documented? |

Availability and Processing Integrity

| Question | Yes / No |

|---|---|

| Are uptime reports available? | |

| Are monitoring alerts documented? | |

| Are restore tests completed? | |

| Are input validation controls evidenced? | |

| Are reconciliation reports available? | |

| Are processing failures reviewed? |

Vendors and Governance

| Question | Yes / No |

|---|---|

| Is the vendor register current? | |

| Is the sub-processor list available? | |

| Are incident response materials ready? | |

| Are policies approved? | |

| Is the risk register current? | |

| Are management review notes available? |

If several answers are “no,” the fintech vendor may not be ready for bank due diligence.

Common Mistakes to Avoid

- Waiting for the bank to ask. Build the evidence bank before the security questionnaire arrives.

- Saying “SOC 2 is in progress” without proof. A roadmap, gap assessment, and evidence tracker are stronger than a vague promise.

- Ignoring API evidence. For fintech vendors, API tokens, scopes, rate limits, and webhooks are critical.

- No Processing Integrity evidence. Banks care whether financial workflows are accurate and traceable.

- Backup evidence without restore testing. Restore testing is stronger than backup reports alone.

- Vendor list without reviews. Banks expect vendor due diligence, not only vendor names.

- Evidence scattered across tools. Use a structured SharePoint evidence workspace.

What Good Looks Like

A strong fintech SOC 2 evidence bank can show:

- SOC 2 roadmap

- scope statement

- control owner matrix

- MFA report

- admin access review

- API token review

- API scope matrix

- rate limit evidence

- webhook security evidence

- data flow diagram

- encryption evidence

- uptime reports

- restore test evidence

- processing integrity checks

- reconciliation reports

- vendor register

- sub-processor list

- incident response tabletop

- change management samples

- logging evidence

- risk register

- bank-ready trust pack

That gives banks confidence. It also helps the SOC 2 audit run more smoothly.

Canadian Cyber’s Take

At Canadian Cyber, we often see fintech vendors wait until a bank asks for evidence before organizing their SOC 2 materials.

That creates pressure.

The better approach is to build a bank-ready evidence bank during SOC 2 readiness.

Banks want clear proof that your fintech platform is secure, available, resilient, governed, and trustworthy.

For fintech APIs and platforms, this means evidence for access, API security, processing integrity, vendor risk, incident response, availability, and leadership oversight. SOC 2 is not only about the final report. It is also about being able to answer serious bank security questions with confidence.

Takeaway

Banks expect fintech vendors to prove security maturity during SOC 2 readiness.

Do not wait until procurement starts. Prepare evidence for:

- SOC 2 roadmap

- access control

- API security

- data protection

- availability

- processing integrity

- vendor risk

- incident response

- change management

- logging

- governance

Then organize everything in a structured evidence workspace. That is how fintech vendors reduce bank review friction, support SOC 2 readiness, and build stronger trust with financial services buyers.

How Canadian Cyber Can Help

Canadian Cyber helps fintech vendors prepare bank-ready SOC 2 evidence.

- SOC 2 readiness assessments

- fintech SOC 2 evidence banks

- bank vendor security review preparation

- API security evidence packs

- access control reviews

- processing integrity control mapping

- availability evidence planning

- vendor risk registers

- sub-processor lists

- incident response planning

- tabletop exercises

- backup and restore evidence reviews

- SharePoint evidence workspace setup

- SOC 2 audit preparation

- vCISO support for fintech security governance

Stay Connected With Canadian Cyber

Follow Canadian Cyber for practical guidance on SOC 2, fintech vendor security, bank due diligence, API security, processing integrity, SharePoint ISMS, vendor risk, and vCISO support.